Walking into a pharmacy with a new prescription can feel like navigating a maze. You hand over the paper, the pharmacist types it in, and suddenly you’re staring at a copay that makes your eyes widen. Why is one medication $10 and another $80? The answer usually lies in how your health plan categorizes drugs, specifically within ACA plans which are health insurance policies sold through the federal or state Health Insurance Marketplaces under the Patient Protection and Affordable Care Act. Understanding this system isn’t just about saving money; it’s about knowing what your coverage actually includes before you need it.

When you buy insurance through the Marketplace, you aren’t just buying a promise of care. You’re signing up for a specific set of rules regarding medications, known as a formulary. This list determines which drugs are covered, which ones require prior authorization, and how much you pay out of pocket. For millions of Americans relying on these plans, the difference between choosing a brand-name drug and its generic equivalent can mean the difference between staying healthy and skipping doses to save cash.

What Is an Insurance Formulary?

An insurance formulary is a curated list of prescription medications covered by a specific health insurance plan. Think of it as a menu. Just as a restaurant menu lists available dishes and their prices, a formulary lists approved drugs and their cost-sharing tiers. If a drug isn’t on the menu, the insurance company generally won’t pay for it, or they’ll pay significantly less.

These formularies are not random. They are developed by committees of doctors and pharmacists who evaluate drugs based on safety, efficacy, and cost. The goal is to steer patients toward treatments that provide the best value. For ACA enrollees, this means that while you have access to thousands of medications, your plan incentivizes certain choices over others through financial structures called tiers.

- Tier 1: Usually low-cost generic drugs. These have the lowest copays, often ranging from $0 to $15.

- Tier 2: Preferred brand-name drugs or higher-cost generics. Copays here might range from $20 to $50.

- Tier 3: Non-preferred brand-name drugs. You typically pay a percentage of the drug’s cost (coinsurance) rather than a flat fee.

- Tier 4: Specialty drugs. These are expensive, often requiring special handling or administration, and carry the highest out-of-pocket costs.

The structure matters because it directly impacts your wallet. A drug placed in Tier 1 is dramatically cheaper than the same drug if it were classified as Tier 3, even if the medical benefit is identical. This tiering system is the engine behind the concept of generic coverage.

The Power of Generic Drug Coverage

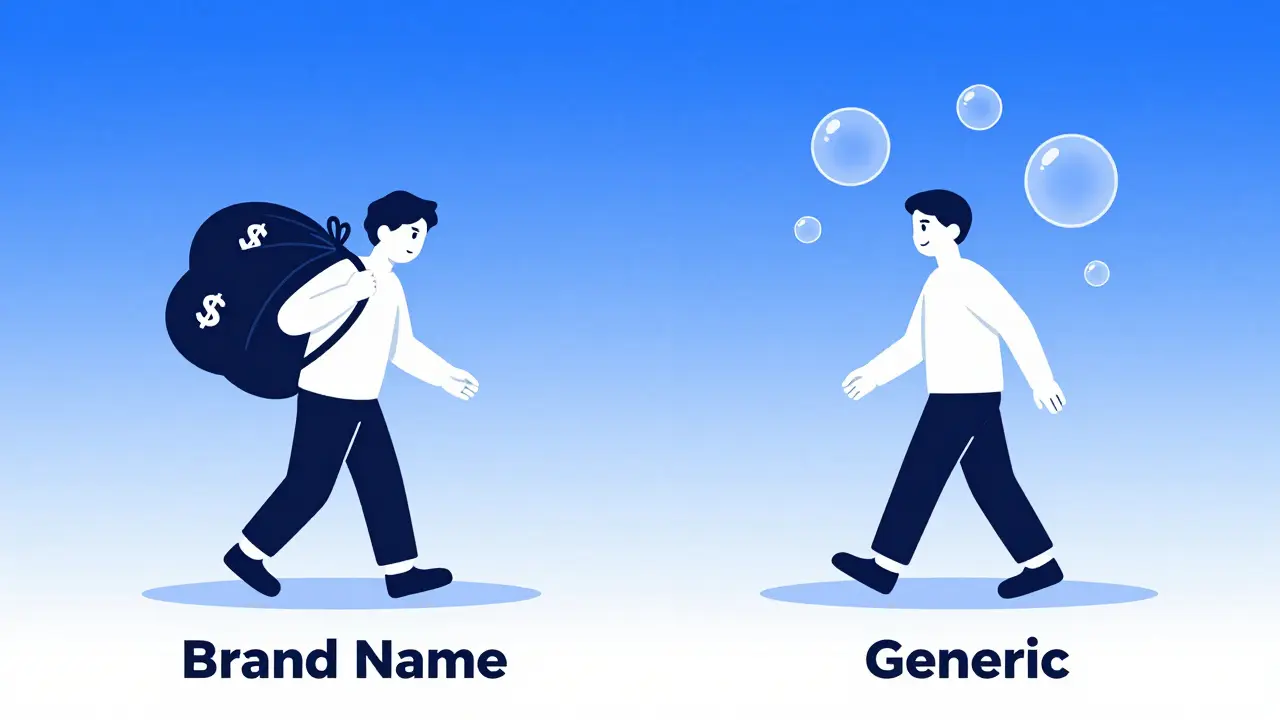

Generic drugs are medications with the same active ingredients, strength, dosage form, and route of administration as brand-name drugs, but sold under a different name at a lower price. When the patent on a brand-name drug expires, other manufacturers can produce generic versions. Because they don’t have to repeat the expensive clinical trials required for the original drug, they can sell it for a fraction of the cost.

In the context of ACA plans, generic coverage is a cornerstone of affordability. Most Marketplace plans place generics in the lowest tier. This encourages both doctors and patients to choose these options whenever possible. For example, if you need a statin for cholesterol, there are dozens of generic options like atorvastatin or simvastatin. Your plan will likely cover these with a minimal copay. However, if you request a newer, brand-name statin that isn’t yet generic, you might face a coinsurance rate of 40% or more.

This dynamic creates a powerful incentive. Let’s say a brand-name drug costs $300 a month. With a 40% coinsurance, you pay $120. The generic version costs $30 a month, and your Tier 1 copay is $10. That’s a savings of $110 per month, or $1,320 a year. Over time, those savings add up, especially for people managing chronic conditions who take multiple medications daily.

| Drug Type | Typical Monthly Price | Patient Copay/Coinsurance | Annual Out-of-Pocket Cost |

|---|---|---|---|

| Brand-Name (Tier 3) | $300 | 40% Coinsurance ($120) | $1,440 |

| Generic (Tier 1) | $30 | Flat Copay ($10) | $120 |

| Savings | -90% | -92% | $1,320 |

It’s important to note that generics are held to strict standards. The Food and Drug Administration (FDA) requires them to be bioequivalent to the brand-name drug. This means they work the same way in the body. Choosing a generic isn’t a compromise in quality; it’s a smart financial decision supported by your insurance plan’s design.

Navigating Metal Tiers and Drug Costs

ACA plans are categorized into metal tiers: Bronze, Silver, Gold, and Platinum. These tiers represent the actuarial value, or the percentage of total average costs for covered services that the plan pays. Bronze plans cover 60%, while Platinum covers 90%. But how does this affect your prescription costs?

Generally, higher metal tiers offer better drug coverage. A Platinum plan might have lower copays for all tiers of drugs, including specialty medications. A Bronze plan, however, often has lower premiums but higher out-of-pocket costs for prescriptions. This is where the trade-off becomes critical. If you take several medications regularly, a Bronze plan might end up costing more in copays than the premium savings provide.

For individuals enrolled in Silver plans, there’s an additional layer of complexity called Cost-Sharing Reductions (CSRs). If your income falls between 100% and 250% of the Federal Poverty Level, you may qualify for CSRs. These subsidies lower your deductibles, copays, and coinsurance for essential health benefits, including prescriptions. In many cases, this means your generic copay could drop to $0. Without understanding this benefit, you might miss out on significant savings simply by choosing the wrong plan type during open enrollment.

Let’s look at a practical scenario. Sarah, a freelance writer earning $32,000 annually, qualifies for a Silver plan with CSRs. Her plan covers her generic blood pressure medication with a $0 copay. If she had chosen a Bronze plan without realizing she qualified for CSRs, she might have paid $15 per fill. Over a year, that’s $180 extra. Conversely, if she had chosen a Gold plan, her premium would have been hundreds of dollars higher each month, outweighing any potential drug savings. The key is matching your expected medical usage with the right metal tier.

Formulary Changes and Prior Authorization

One of the most frustrating aspects of insurance is when a drug you’ve been taking suddenly disappears from your formulary. Insurers update their formularies regularly, often adding new drugs and removing older ones. Sometimes, a drug is removed entirely. Other times, it’s moved to a higher tier, meaning your copay goes up.

If your doctor prescribes a drug that isn’t covered, or is only covered under specific conditions, you may encounter prior authorization is a process where your doctor must get approval from your insurance company before they will cover a specific medication or service. This happens when the insurer wants to ensure that the drug is medically necessary and that cheaper alternatives have been tried first. It can cause delays in treatment, which is stressful for anyone dealing with a health issue.

To avoid surprises, check your plan’s formulary before you start a new medication. Most insurers provide online tools where you can search for a drug and see its tier status. If your current drug is being phased out, talk to your doctor early. They may be able to switch you to a similar generic option that remains on Tier 1. Proactive communication can prevent gaps in coverage and unexpected bills.

Specialty Drugs and High-Cost Medications

Not all medications fit neatly into the generic vs. brand-name binary. Some drugs, particularly those used to treat complex conditions like cancer, rheumatoid arthritis, or multiple sclerosis, are classified as specialty drugs. These medications often require special handling, such as refrigeration, or must be administered via injection or infusion. They are almost always placed in the highest tier of the formulary.

For these drugs, copays can be substantial. While a generic pill might cost $10, a specialty drug could result in a bill of $1,000 or more per month. Many ACA plans include specific caps or assistance programs for specialty drugs, but the details vary widely. It’s crucial to understand whether your plan offers a hard cap on out-of-pocket costs for these medications or if you’ll continue paying high coinsurance until you hit your annual out-of-pocket maximum.

Pharmaceutical companies often provide patient assistance programs (PAPs) for high-cost drugs. These programs can reduce the cost significantly, sometimes to zero, regardless of your insurance status. However, accessing these programs can be bureaucratic. Your doctor’s office or the pharmacy should help you navigate this process. Don’t assume your insurance is the only source of funding for expensive medications. Exploring PAPs can be a lifeline for those facing steep bills.

Maximizing Your Benefits

Getting the most out of your ACA plan’s drug coverage requires a bit of effort. Here are some actionable steps to keep your costs down:

- Review Your Formulary Annually: During open enrollment, don’t just pick the cheapest premium. Check if your regular medications are still covered and what tier they’re in.

- Ask for Generics: Whenever possible, ask your doctor if a generic alternative exists. Most of the time, the answer is yes.

- Use Mail-Order Pharmacies: Many ACA plans offer discounted rates for 90-day supplies of maintenance medications sent via mail. This can save you money and ensure you never run out.

- Understand Your Subsidies: If you’re on a Silver plan, confirm whether you qualify for Cost-Sharing Reductions. This can drastically lower your prescription costs.

- Appeal if Necessary: If your insurer denies coverage for a drug you believe is medically necessary, you have the right to appeal. Gather documentation from your doctor supporting the need for the specific medication.

Knowledge is power when it comes to healthcare. By understanding how formularies work, the role of generics, and the nuances of your specific plan tier, you can make informed decisions that protect both your health and your finances. The Affordable Care Act was designed to make coverage accessible, but maximizing its benefits requires active participation from you.

Does every ACA plan cover generic drugs?

Yes, all ACA Marketplace plans are required to cover essential health benefits, which include prescription drugs. Generics are typically placed in the lowest cost tier, making them affordable for most enrollees. However, the specific copay amount varies by plan.

What happens if my drug is not on the formulary?

If your drug is not on the formulary, your insurer may deny coverage. You can ask your doctor to prescribe a therapeutic alternative that is covered, or you can request a formulary exception. An exception allows the insurer to cover a non-formulary drug if it is deemed medically necessary.

Are generic drugs as effective as brand-name drugs?

Yes. The FDA requires generic drugs to be bioequivalent to their brand-name counterparts. This means they contain the same active ingredient, work in the same way, and have the same dosage form and strength. The main differences are usually in inactive ingredients and price.

How do Cost-Sharing Reductions affect my drug costs?

Cost-Sharing Reductions (CSRs) lower your deductibles, copays, and coinsurance for essential health benefits, including prescriptions. If you qualify for CSRs and enroll in a Silver plan, your copay for generic drugs may be reduced to $0.

Can I appeal a drug denial?

Yes. If your insurer denies coverage for a medication, you have the right to file an appeal. You will need to provide medical evidence from your doctor explaining why the specific drug is necessary and why alternatives are not suitable. Appeals can be internal (with the insurer) or external (with an independent review organization).